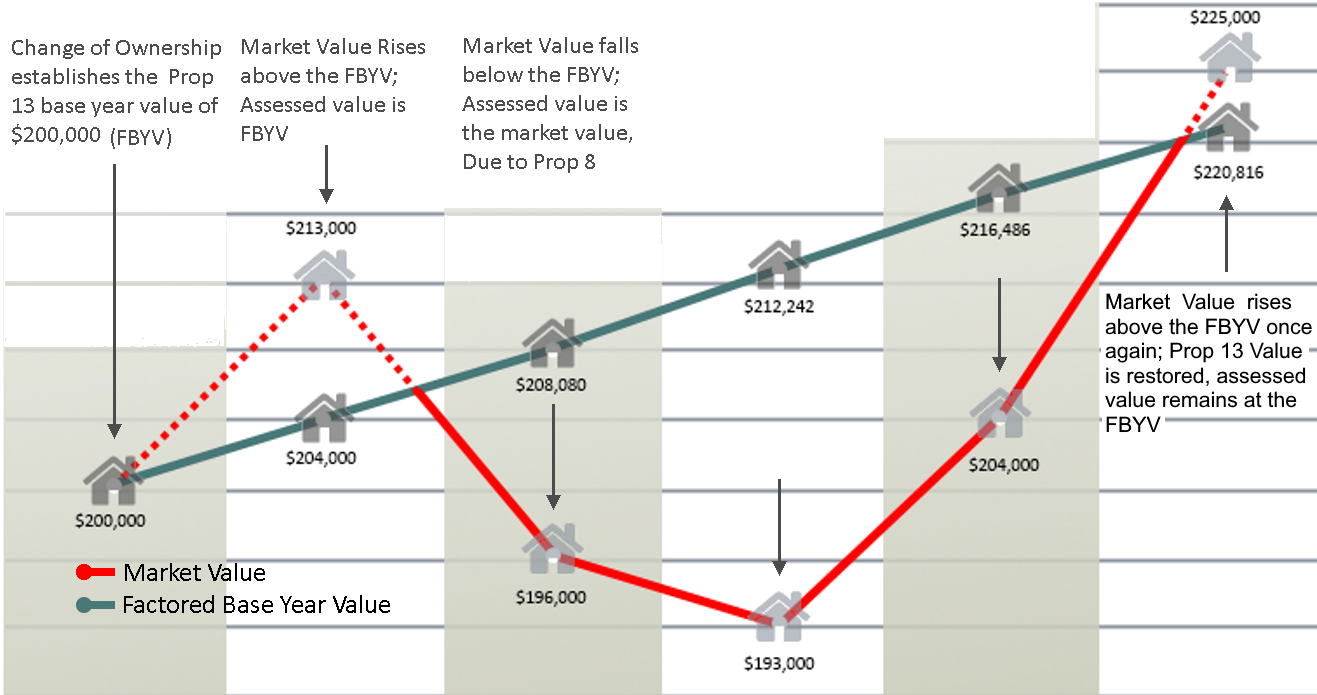

In 1978, California voters passed Proposition 8, a constitutional amendment that allows a temporary reduction in assessed value when real property suffers a decline in value. A decline in value occurs when the current market value of real property is less than the current factored base year value (i.e., Prop. 13 value) as of January 1.

A decline in value may result from changes in the real estate market, the neighborhood or the property itself. When a property’s market value exceeds its factored base year value (FBYV), the Assessor must return the taxable value to its FBYV.

Prop. 8 assessments can be the outcome of assessment appeals, informal petitions to the Assessor or Assessor-initiated reviews.

Temporary decline in taxable value

Real property is typically assessed at the lesser of two values:

FBYV, according to Prop. 13 (most often the purchase price adjusted annually for inflation, not to exceed 2% per year)

Fair market value according to Prop. 8 as of January 1

When the market value is the lesser value, the property is placed in decline-in-value status (Revenue and Taxation Code § 51). When a property is in decline-in-value status, its assessment is reviewed annually. As the real estate market fluctuates, the property's assessed value may rise or fall accordingly, reflecting changes in market conditions.

For example, an assessed value may:

Decrease based on current market data, such as comparable sales, rents and capitalization rates

Increase based on current market data, but not more than the FBYV.

Maintain the assessed value from the prior year.

Be restored to its current FBYV.

Prop. 8 values may increase by more than 2%

Real property assessments in decline-in-value status may increase as the real estate market recovers, even beyond the 2% limit set by Proposition 13. While Prop. 13 limits annual increases of FBYV to 2%, this cap does not apply to properties in decline-in-value status. When the market value of a property as of January 1 exceeds the factored base year value, the FBYV becomes the new taxable value for the upcoming roll year, effectively ending the property's decline-in-value status.

Prop. 13 vs. Prop. 8 valuation:

Proposition 13 (Prop. 13) limits annual property tax increases to 2% per year. When a property's market value is less than its Prop. 13 assessment, Proposition 8 (Prop. 8) allows for temporary tax relief based on its current market value as of Jan. 1.

However, when the market value rises, the assessment is permitted to rise more than 2%.

On June 6, 1978, California voters overwhelmingly approved Proposition 13, a property tax limitation initiative. This amendment to California’s Constitution was the taxpayers’ collective response to dramatic increases in property taxes. Prior to 1978, real property was appraised cyclically, with no more than a five-year interval between reassessments, keeping assessed values at or near current market value levels.

Prop. 13 created an acquisition-based tax system that limits the annual assessment growth of real property to 2% or the rate of inflation, whichever is lower. Taxable values of real property are established or modified only when taxable property is sold or newly constructed. As a result, two identical properties can have different assessed values depending on when they were purchased. These restrictions allow property taxes to be predictable for owners of real estate and for entities that rely on tax dollars for funding.

Prop. 13:

Rolled back local real estate assessments to 1975 market value levels.

Set the maximum tax rate at 1% of a property’s market value at the time of acquisition, with an allowance that the rate may exceed 1% to repay voter-approved debt, such as local school and hospital bonds.

Adjusts taxable values for inflation, but limits the annual increase to no more than 2% per year.

Provides that property is reassessed when there is new construction or change of ownership.

Requires a vote of at least two-thirds of the State Legislature for approval of new state taxes, and support of at least two-thirds of local voters for approval of local taxes earmarked for special purposes. This requirement was modified when California voters approved Proposition 39 in 2000, lowering the threshold specifically for school bonds. Under Prop. 39, local school districts, community college districts, and county education offices can pass school bonds with a 55% voter approval, instead of the original two-thirds requirement, provided certain conditions are met. These conditions include:

A clear list of projects to be funded by the bond

Annual audits to ensure the money is spent as intended

This reduced voting threshold applies specifically to bonds for school facility construction and improvements.

A citizens’ oversight committee to monitor the spending

The Assessor mails annual valuation notices to inform property owners of their properties' taxable values as of January 1. The assessed value is used to calculate the property taxes due for the upcoming year. Notices are mailed when the assessed value changes—due to a change in ownership, new construction, or a decline in value. However, no notice is sent when the change results from the annual inflation adjustment under Proposition 13.

For properties in decline-in-value status, the taxable value shown in the notice reflects the property’s current market value. To calculate the tax break, subtract the taxable value from the Factored Base Year Value, which represents the maximum taxable value allowed by law.

Compare the taxable value on your notice with last year’s tax bill

Does the total taxable value exceed the fair market value of your property? If so, contact the Assessor's Office to request a value review.

Did the taxable value increase by more than 2% from the previous year? If so, your property may be in decline-in-value status, and its value has been updated by the Assessor to reflect current market conditions. Remember, the 2% cap on annual increases under Proposition 13 doesn’t apply to market value assessments under Proposition 8.

If your taxable value increased by more than 2% and your property is not in decline-in-value status, the increase could reflect construction in progress. Contact the Assessor's Office for clarification.

If you disagree with your assessment, contact the Assessor’s Office to discuss the valuation. If you still disagree after that, you may wish to file an assessment appeal with the Clerk of the Board of Supervisors.